Forward Property Price Index

The WhenFresh Forward Property Price Index gives mortgage lenders the means to re-assess the values and LTVs of the properties within their portfolio quickly, cost-effectively and at scale – to drive faster, better mortgage decisions.

WhenFresh Forward Property Price Index

> Overview

The data science team at WhenFresh has created the Forward Property Price Index to provide UK mortgage lenders with the means to quickly and cost-effectively review changes to the values of the properties within their mortgage portfolios more accurately than ever before – at scale.

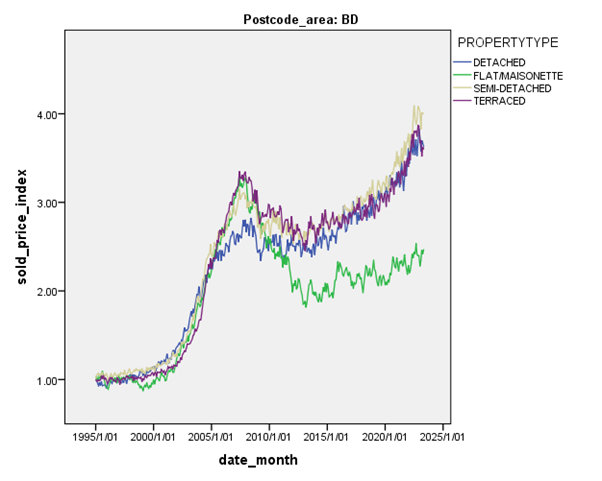

Standard house price indices such as that produced by the Land Registry show broad macro-economic trends across relatively few, very large geographical regions, and are not a sufficiently detailed or reliable indicator of changes in different types of properties at a local level.

In contrast, the WhenFresh Forward Property Price Index has been designed to provide a highly granular view of the changes in values of different types of properties within over 120 micro-geographies, thereby giving accurate and actionable results upon which lenders rely to base mortgage lending decisions.

To illustrate this, the graph below shows the relative performance over time of certain property types in the BD postcode area, where flats have performed very differently to houses:

(View/Download Technical White Paper here…)

The Forward Property Price Index enables a mortgage lender to quickly, accurately and inexpensively analyse the individual property values and LTVs within their existing mortgage portfolio and re-assess risk.

By combining these insights with knowledge of their borrowers’ payment histories, lenders can now selectively make timely new fixed rate mortgage offers to their existing customers, as their current fixed term deals near their expiry, for example.

> The problem

For many borrowers, 2023 may well produce the “perfect financial storm”.

Firstly, more fixed-rate mortgage deals are due to reach the end of their term in 2023 than has been the case in each of the previous 20 years. Estimates vary, but close to 2 million borrowers are going to have to either accept their current lender’s variable rate or to try and secure a new fixed rate deal either with their existing lender, or a different one.

However, with the UK in the grip of a cost-of-living crisis, with high inflation and volatile, rising interest rates, millions of borrowers are already finding it harder to make ends meet.

These factors make it ever more difficult for borrowers to even qualify for and/or afford a new mortgage or remortgage. Then there’s the mortgage application process itself – which can be a costly and time-consuming process.

All in all, large numbers of borrowers therefore face being forced to spend precious time and money shopping around for mortgages that will likely be more difficult to get and harder to afford.

> The WhenFresh Solution

There is one bit of good news for borrowers though – in that the regulators have acted to relax the affordability rules for borrowers who are staying with their existing lender when their fixed term deal expires – and this is where the WhenFresh Forward Property Price Index can really support mortgage lenders.

Any lender will of course know when each of their customers will reach the end of their fixed-rate mortgage term. They can also see each borrowers’ payment history and assess consumer credit risk, with the support of credit bureau data as needed.

What the lender doesn’t yet know is what has happened to the value of each property on its books and therefore where the LTV will stand when a borrower’s fixed rate deal expires.

The lender does of course also know the details of the property valuation when any given mortgage was issued, such as the date and type of valuation, the property address/postcode, type, bedroom count at the time etc.

By providing these details and applying the WhenFresh Forward Property Price Index, the lender can obtain an instant, accurate and inexpensive current property valuation, without the cost and time that would be involved in arranging a new, physical valuation.

Moreover, the Forward Property Price Index enables the lender to do all of this very quickly, very inexpensively, and at scale.

This means lenders can now analyse their current fixed-term portfolios and identify borrowers with good payment histories, in properties where the current valuation and LTV all pass lending criteria, to selectively offer new, competitive fixed-term deals to their existing customers.

> Key Benefits of the WhenFresh Forward Property Price Index

The key benefit to a lender is that they can now very quickly and inexpensively reassess the current valuations and LTVs across segments of their mortgage portfolios, at scale.

Based on these unprecedented insights, the lender can selectively make attractive new fixed-rated offers to their existing borrowers, to increase customer retention.

The borrowers benefit as the process is very simple and frictionless. They don’t have to the spend time and money shopping around for a new mortgage that they may find harder to get, or incurring costs for mortgage processing, or a physical property valuation/survey visit.